Truck drivers can claim an overnight allowance of 8 Euro per calendar day as business expenses - in addition to the "normal" meal allowance. This applies to the day of arrival or departure and each calendar day with an absence of 24 hours during an off-site activity in Germany or abroad (§ 9 Abs. 1 Satz 3 Nr. 5b EStG, introduced by the "Act on Further Tax Promotion of Electric Mobility and Amendment of Other Tax Regulations").

The Federal Fiscal Court has recently ruled that the area of operation for an industrial railway train driver constitutes a main place of work and not a large-scale work area (BFH ruling of 1.10.2020, VI R 36/18).

The Federal Fiscal Court has recently ruled that the depot is not the main place of work for a refuse collector if they only listen to the tour management announcement, collect the logbook, vehicle documents and keys, and check the vehicle lighting there (BFH ruling of 2.9.2021, VI R 25/19).

(2022): What can be deducted for work on a vehicle?

What should I know about the new 48-month limit?

For off-site work, travel, accommodation, and incidental travel expenses, as well as meal allowances, can be deducted as business expenses.

Since 2014, a new 48-month limit has played a significant role.

(1) The 48-month limit in determining the first place of work

"First place of work" is a fixed workplace of the employer to which the employee is permanently assigned. Even without an explicit designation by the employer, a permanent assignment is assumed if the employee is to work at a location for an extended period. This is the case for employment

- for an indefinite period ("until further notice"),

- for the entire duration of the employment contract (fixed-term or indefinite) or

- for a period of more than 48 months.

TIP: This means: All assignments (transfers, secondments, postings) that are initially limited to a maximum of 48 months do not constitute a "first place of work" but off-site work. Therefore, travel costs can be deducted with the business travel allowance or the actual costs, as well as meal allowances and accommodation costs as business expenses or reimbursed tax-free by the employer.

(2) The 48-month limit for work at a customer's premises

Unlike in the past, an employee can now have their "first place of work" at a customer's premises of their employer, but only for long-term work. This applies, for example, to employees who work on a long-term project at the customer's site or temporary workers who work for the hirer without a time limit.

Such long-term work exists if the employee works at a customer's premises or a related company

- from the outset for more than 48 months or

- for the duration of the employment contract.

(3) The 48-month limit for accommodation costs

For overnight stays during off-site work, only the actual costs can be deducted as business expenses or operating costs. Since 2014, accommodation costs can only be deducted in full or reimbursed tax-free by the employer for a period of 48 months.

From the 49th month, the deduction of business expenses or tax-free reimbursement is limited to comparable expenses for double housekeeping, i.e. to a maximum of 1.000 Euro per month. This limit only applies to off-site work in Germany, not abroad.

Tipp

The 48-month period starts anew if the work at the same place of work is interrupted for at least 6 months. The reason for the interruption (e.g. illness, holiday, work at another place of work) does not matter.

The Münster Finance Court has recently confirmed the tax authorities' view and ruled that repeatedly limited assignments to a construction site of less than 48 months each do not establish a "first place of work" there, even if the assignment lasts continuously for more than four years (Münster Finance Court, 25.3.2019, 1 K 447/16).

Special case for temporary workers:

Temporary workers are not in an employment relationship with the company where they are deployed, but with "their" temporary employment agency, often referred to as the "lender". If these employees are "lent" to a specific company for a certain period, the question arises whether they can deduct their travel to the place of work according to travel expense principles (30 cents per kilometre travelled) or only with the lower commuting allowance (30 cents per kilometre of distance).

In principle, travel costs can only be claimed with the commuting allowance if the temporary worker is permanently assigned to a place of work. This is the case if they are to work there for an extended period, namely

- for an indefinite period ("until further notice"),

- for the duration of the employment contract or

- for more than 48 months.

This means: Temporary workers can also have their "first place of work" at the customer's site if they work there for an extended period. However, this is only the case if the employee is to work there from the outset (!) for more than 48 months or for the duration of the employment contract or indefinitely. Travel can then only be deducted with the commuting allowance, and meal allowances and incidental travel expenses are not taken into account. Temporary workers who work at customers' premises for a shorter period, however, are engaged in off-site work and can therefore claim their travel with the business travel allowance - and to a certain extent also meal allowances.

SteuerGo

The Lower Saxony Finance Court recently ruled that an employee in a permanent employment relationship with a temporary employment agency can only claim travel costs with the commuting allowance for their journeys between home and place of work, even if the temporary employment agency has agreed on a fixed term for the work with the respective hirer of the employee (judgment of 28.5.2020, 1 K 382/16).

However, the Federal Fiscal Court overturned the judgment (Federal Fiscal Court judgment of 12.5.2022, VI R 32/20). According to this, the relevant employment relationship for the question of whether the employee is permanently assigned to a company facility within the meaning of Section 9 (4) sentences 1 to 3 of the Income Tax Act is the employment relationship between the employer (lender) and the (temporary) employee. If the employee's assignment to the hirer consists of repeated but fixed-term assignments, there is no permanent assignment.

In its judgment of 10.4.2019 (VI R 6/17), the Federal Fiscal Court stated that the existence of a fixed-term temporary employment relationship does not preclude the assumption of a permanent assignment. However, it did not have to decide the case specifically, as in the case at hand, the employee was assigned to two different places of work in succession during their employment. This was not the case in the current situation, as the claimant was in fact only employed by company B and had been hired specifically for this purpose by the temporary employment agency. In any case, the Federal Fiscal Court is now involved again, as the appeal is pending (Ref. VI R 32/20). Affected temporary workers should therefore appeal against negative tax assessments and request that their own proceedings be suspended.

(2022): What should I know about the new 48-month limit?

What applies to business trips abroad?

There are some special tax regulations for off-site work abroad:

(1) Meal allowances: These vary depending on the country. Special rates are set for particularly expensive cities. The allowances are derived from the Federal Travel Expenses Act and are periodically updated by the Federal Ministry of Finance.

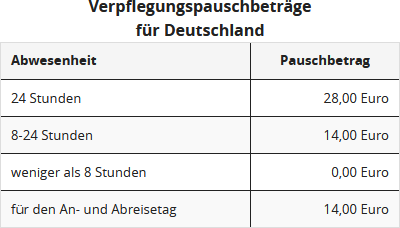

- For each full day of absence, the country-specific meal allowance is 120%, and for days with an absence of more than 8 hours as well as on arrival and departure days, it is 80% of the highest foreign daily allowances.

(2) In-flight meals: In-flight meals are usually included in the flight price. If the invoice for the flight ticket is issued to the employer and reimbursed by them, the following applies:

The free in-flight meal is considered a "meal provided by the employer". This means that the meal allowance must be reduced by 40% for lunch or dinner and by 20% for breakfast. The reduction of the meal allowance does not apply if it is clear from the chosen fare that it is purely a transport service with no free meals provided.

(3) Multiple countries: If you visit several countries during your off-site work, the meal allowance is always based on the country you reach last before 24:00 local time. On the return day, the country where you last worked is decisive - not Germany. This also applies if you continue your off-site work in Germany, for example, by visiting a customer in Germany.

(4) Overnight allowances: For overnight stays abroad, the country-specific overnight allowances can no longer be deducted as business expenses but can only be reimbursed tax-free by the employer. If off-site work abroad lasts longer than four years, there is no limit on deductible accommodation costs to 1.000 Euro per month for the 48 months, unlike in Germany.

SteuerGo

Current decision by the Federal Fiscal Court: meal allowances must also be reduced for employees without a "primary workplace" if the employer provides them with free meals (BFH ruling of 12.7.2021, VI R 27/19).

The case: A ship's officer receives free meals on board from the employer. In the payroll statements, the employer showed these meals as tax-free benefits in kind. On "port days", the officer did not always use the provided on-board meals. On some days, the crew had to cater for themselves in ports. The officer claimed meal allowances for 206 days as business expenses.

According to the BFH, the officer is only entitled to meal allowances for the days when the employer did not provide him with meals on port days. For all other days, the deduction is excluded, as breakfast, lunch, and dinner were provided free of charge on those days.

SteuerGo

Current decision by the Düsseldorf Finance Court: no taxable wages are granted to flight personnel through the provision of meals if the flight lasts longer than six hours (ruling of 13.8.2020, 14 K 2158/16 L). The case: An airline provided its flight personnel with free meals on long-haul flights and on medium-haul flights when the flight time with short "turn-around times" exceeded six hours.

These were apparently typical catering meals. The tax office argued that the free provision of meals was taxable wages. However, the corresponding lawsuit was successful. Reason: The free meals were provided predominantly in the employer's operational interest. They were not a reward for the personnel's work performance.

The extraordinary working conditions on board an aircraft, characterised by the tight schedule in air traffic and the cramped environment in the aircraft, had to be taken into account. The provision of meals primarily served to ensure a smooth and efficient process during flight times and "turn-around times". Furthermore, the judges stated that the airline was legally obliged to provide the crew with the opportunity to have meals and drinks if the flight duty time exceeded six hours.

(2022): What applies to business trips abroad?

What applies when meals are provided by the employer?

During off-site activities, such as training events, seminars, conferences, sales events, etc., participants are often provided with meals at the employer's expense, either directly by the employer or at their instigation by a third party, e.g. the conference hotel or a catering company.

The beneficiary is taxed by the authorities for this benefit.

The relevant meal allowance is reduced. The reduction is 20% for breakfast and 40% for lunch or dinner of the full meal allowance. Taxation at the official rate for benefits in kind only occurs if the employee cannot claim meal allowances as business expenses, e.g. for an absence of less than 8 hours or for a long-term off-site activity after the three-month period. The limit for "standard catering" is 60 Euro.

SteuerGo

Current Federal Fiscal Court has ruled that meal allowances must also be reduced for employees without a "primary place of work" if the employer provides them with free meals (BFH ruling of 12.7.2021, VI R 27/19).

The case: A ship's officer receives free meals on board from the employer. In the payroll statements, the employer showed these meals as tax-free benefits in kind. On "port days", the officer did not always take advantage of the on-board meals provided. On certain days, the crew had to cater for themselves in ports. The officer claimed meal allowances for 206 days as business expenses.

According to the BFH, the officer is only entitled to meal allowances for the days on which the employer exceptionally did not provide meals on port days. For all other days, the deduction is excluded, as breakfast, lunch, and dinner were provided free of charge on those days.

(2022): What applies when meals are provided by the employer?